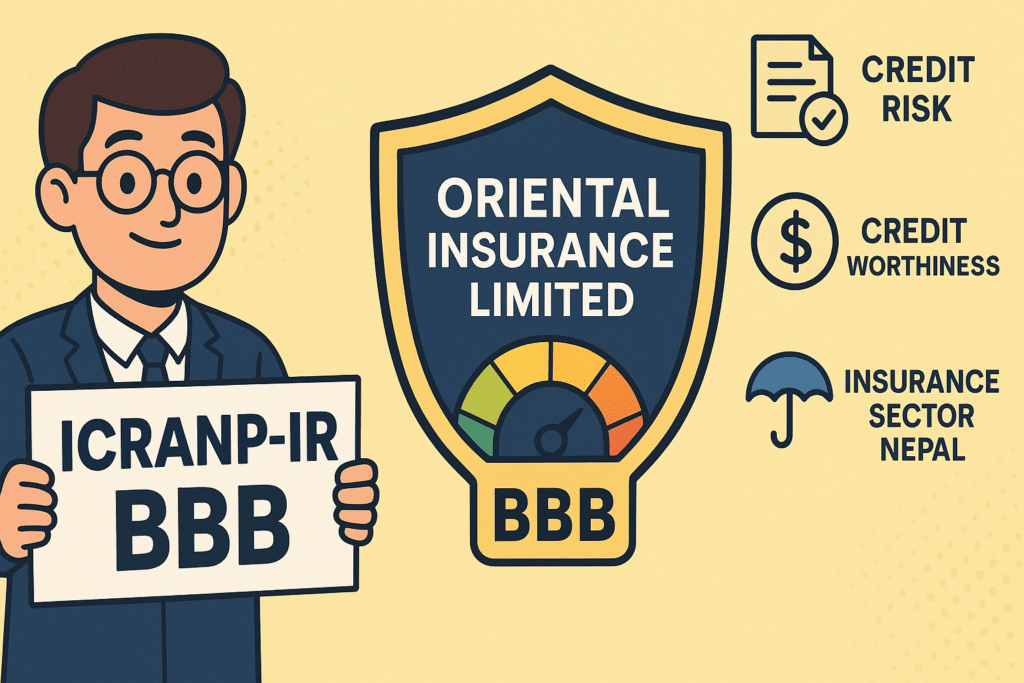

Siddhartha Premier & Oriental Insurance: ICRA Nepal Assigns ICRANP-IR BBB Issuer Rating

ICRA Nepal Limited has assigned Oriental Insurance Limited an issuer rating of ICRANP-IR BBB, signalling a moderate level of safety in meeting its financial obligations and a Moderate credit risk. This issuer rating reflects the company’s overall creditworthiness and is not linked to any single debt instrument. What the ICRANP-IR BBB Rating Means This rating […]